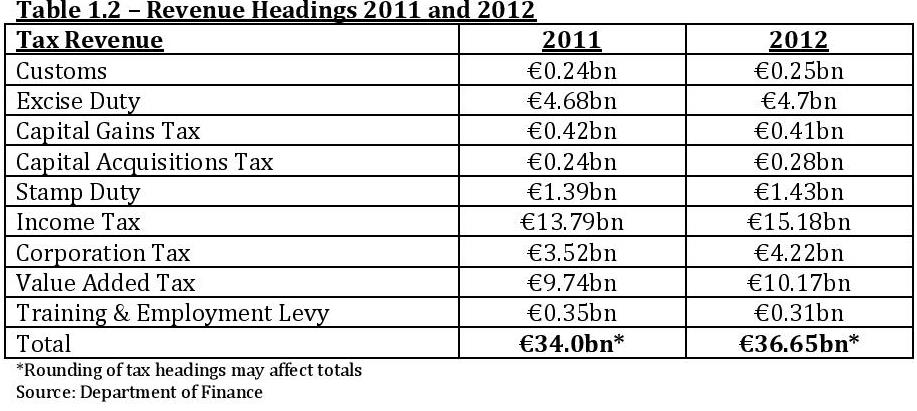

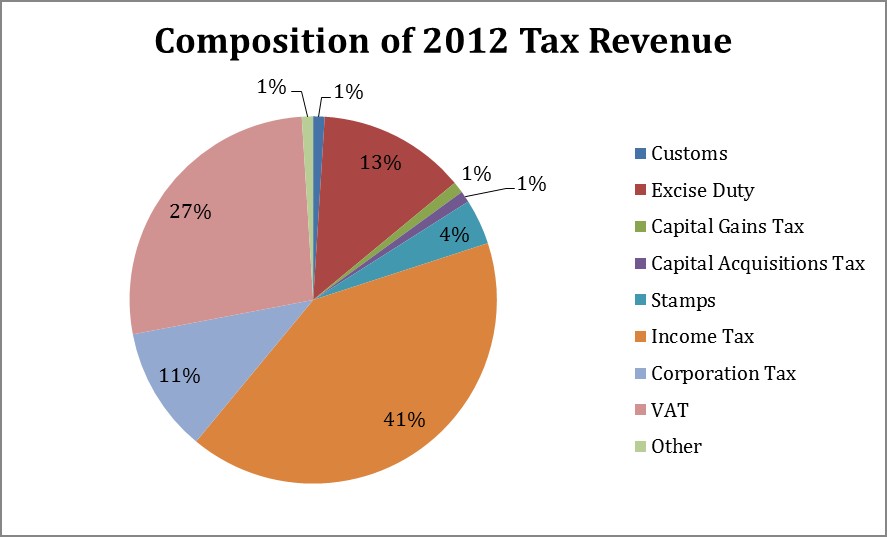

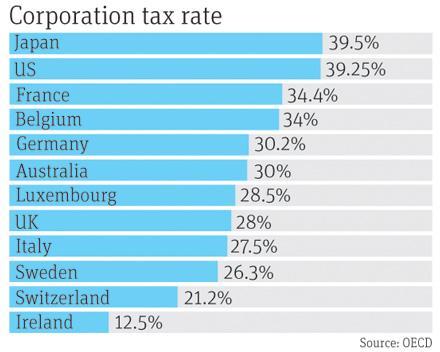

In 2012 the Irish government received �4.2bn

in corporation tax and �15.18bn in income tax.

Advanced Tax Agreements (ATAs)

Glanbia�s �1bn Luxembourg move

to cut its Irish tax bill

(The Irish Times)

More than 340 firms got tax

deals from Luxembourg, leaked documents show

Irish food multinational Glanbia has put more than �1

billion into companies in Luxembourg that have no employees

but serve to reduce its tax bill here.

The companies are the subject of advanced tax agreements (ATAs)

negotiated with the tax authorities in Luxembourg and

feature in 28,000 pages of leaked documentation from

PricewaterhouseCoopers (PwC) in Luxembourg detailing ATAs

with multinational companies around the globe.

The leaked documents have been shared by the Washington

DC-based International Consortium of Investigative

Journalists (ICIJ) with more than 40 media groups around the

world, including The Irish Times.

The leaked documents show how Pepsi, Ikea, FedEx and 340

other companies secured tax deals from Luxembourg, allowing

many of them to slash their tax bills while maintaining

little presence in the tiny European Union member state.

The material also shows how foreign multinationals use

Ireland as part of Luxembourg- based structures that reduce

their corporation tax bills in the Republic and elsewhere.

Transactions covered by the ATAs include cross-border loans

that create interest costs that can be charged against tax

outside Luxembourg but which create relatively tiny tax

charges in Luxembourg.

The Organisation for Economic Co-operation and Development

has noted in a recent report on global tax change that

$1,987 billion went into Luxembourg special-purpose entities

� companies that often have few if any employees � as part

of global financing and tax planning structures. Most of the

money came straight back out again.

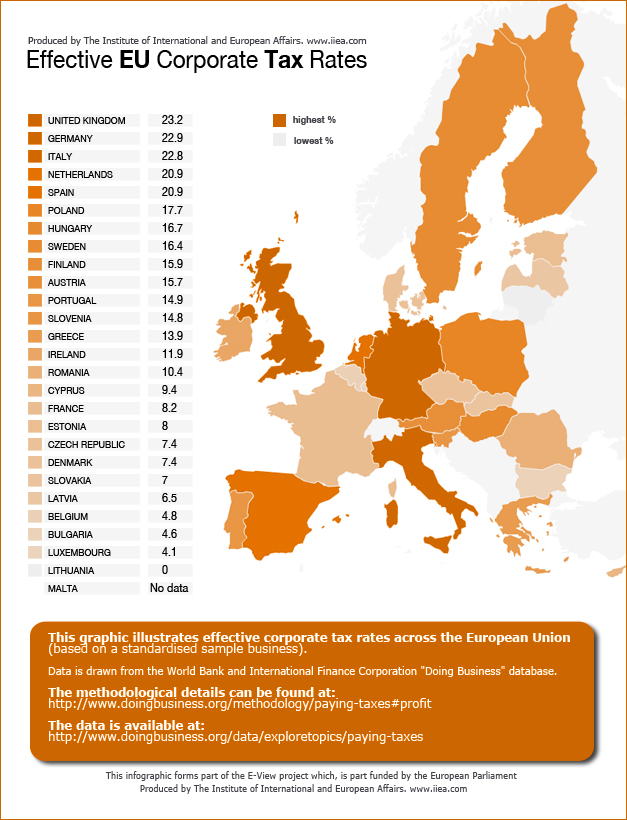

"Effective corporate tax, like effective

income tax, is the rate which is paid once reliefs, allowances,

exemptions and depreciation is taken into account.

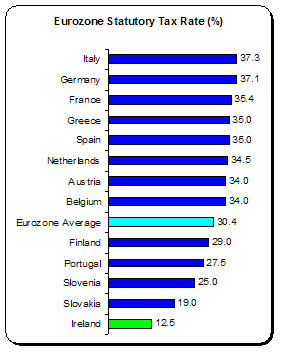

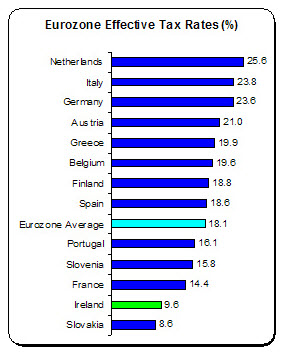

The average corporate tax rates � over 30 percent statutory � falls to

18 percent effective.

For example, France falls from over 35 statutory

percent to 14 percent effective � nearly a 50 percent fall. France is

below the Eurozone average."

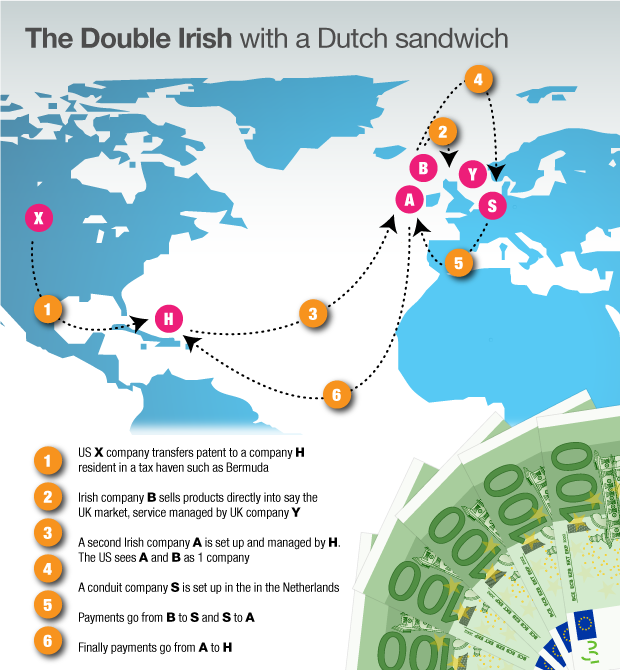

"Leading US senators push Irish

government to fully tax Apple, Google etc.

Ireland's days as a tax haven for American tax companies, such as

Apple, Google and Facebook, may soon end if US senators get their way.

The chairman of the Senate Permanent Subcommittee on Investigations,

Carl Levin (D-Mich.), and Sen. John McCain (R-Ariz.) are again

attempting to curtail the �Double Irish and Dutch Sandwich�

tax-avoidance scheme (in which American-owned companies use Irish and

Dutch subsidiaries to funnel profits into low- or no-tax jurisdictions)

The proposed policy change would move Ireland a step closer to fully

charging companies its official 12.5 percent corporate tax rate.

Loopholes frequently lower the tax rate to around 3 percent.

�The US government is losing tens of billions of dollars at a time when

we are revenue-constrained, worrying about the deficit, cutting spending

� you know, we need all the money we can get,� said economist Bruce

Bartlett, a former domestic policy adviser to Ronald Reagan.

The Double Irish utilizes loopholes in US and Irish tax laws to move

profits of US multinationals from Ireland to jurisdictions with zero

corporate-tax rates, such as Bermuda.

The so called Dutch sandwich shifts profits in Ireland through the

Netherlands en route to Bermuda.

The Post reports that Audit Analytics notes that major US companies

pumped up their offshore earnings by 15 percent last year to a record

$1.9 trillion by posting profits outside the US and avoiding a huge tax

bill."

Ireland is world's fourth most expensive

for petrol

[A] report, by Louth accountants, UHY

Farrelly Dawe White, also found that Irish diesel prices are the fifth

highest in the world.

It costs about �139 to fill the tank of a Ford Transit with petrol in

Denmark; in Ireland, it costs about �128. The cheapest place to buy

petrol is the United Arab Emirates (UAE) followed by Malaysia, Mexico

and the US. It costs �27 to fill up a tank with petrol in the UAE, �37

in Malaysia, �52 in Mexico and �55 in the US.

Taxes account for almost 60 per cent of the cost of filling up the tank

of a Ford Transit with petrol in Ireland, compared to about 13 per cent

in the US. There are no fuel taxes in China or Malaysia.

A typical Irish driver pays about �2,754 a year in fuel and �1,652 of

this is tax.

A spokeswoman for the Department of Finance said fuel prices are driven

by several factors "including the price of oil on international markets,

exchange rates, production costs and refining costs".

Tax hikes drive price of petrol and

diesel up European league table

A survey of 27 countries carried out this

month by the Automobile Association (AA ) found that drivers in Norway

pay the most for a litre of petrol � �1.92 � despite owning all the

North Sea oil off their shores.

They are followed by the Netherlands (�1.86), Italy (�1.81), Sweden

(�1.77) and Greece (�1.72). Poland had the cheapest fuel at the

forecourt, charging its drivers just �1.32 a litre, closely followed by

Latvia (�1.34), Estonia (�1.36) and Luxembourg (�1.37).

Our nearest neighbours in the UK pay slightly more, forking out �1.61

for every litre they buy. Ireland is in 12th place. The price of petrol

and diesel crept upwards at the pumps this month for the first time

since last September.

AA corporate affairs spokesman Conor Faughnan said: "We used to have the

cheapest petrol in Europe in 2008. But since October that year, the

various government taxes have added 23c onto a litre of petrol."

"In countries like Norway they have higher fuel taxes, but they don't

have the full range of motor taxes we have, such as VAT, insurance levy,

Vehicle Registration Tax, tolls, motor tax. We have them all."

The Government Should now Come Clean on

Water Charges

November 05, 2014

Michael Taft, Research Officer, UNITE the Union

I admit I can�t let this issue go but such is the misrepresentation,

partial information and deliberate obfuscation being put out in the

debate that it goes beyond a narrow calculation. It actually reveals a

Government determined to hide the facts in pursuit of a policy which

caused over 150,000 to demonstrate last weekend.

Yes, I�m talking about water charges � but specifically about the

estimated impact on the deficit if water charges were removed. And now

Dr. Tom McDonnell over at the Nevin Economic Research Institute has done

his own sums � and they mirror what I had previously calculated here.

The Government is claiming that removing the water charges would �cost�

�800 million (this was run out again on Morning Ireland today). Is this

correct? No. Let�s look at how the Government is obscuring the real

numbers and see if we can find the right ones. If this gets a little

�number-dense� please stay with it for it is about more than just

abstract calculations; it is about how the Government is treating this

issue and the public at large. All numbers are approximate and rounded.

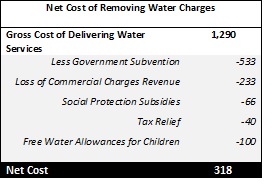

I have produced a summary table below.

First, the total cost of water service provision is �1.3 billion (�700

million in current spending and �600 million in investment).

Second, the Government is committing �500 million from the Local

Government Fund to Irish Water. This is �on the books�; that is, this is

counted as government expenditure.

Third, this leaves a saving to the Government of �800 million.

So far, pretty clear. The Gvvernment's argument seems to stack up. But,

no, this is not the case. Because the Government is losing �250 million

in revenue. This is the amount collected through commercial water

charges on businesses This used to Government coffers. Now it belongs to

Irish Water.

So the Government gains �800 million savings on the expenditure side but

loses �250 million on the revenue side. This leaves a saving of

approximately �550 million. This is pretty much the same number that Dr.

McDonnell arrives at: �527 million.

Ok, so we have sorted that out. The actual cost of removing water

charges would be �550 million � yes? No, that's not it either. Because

the Government is spending money as part of the move to water charging �

spending that wouldn�t exist if there weren�t the charges. Dr. McDonnell

states that he doesn�t factor these in. So let�s do that. There are

three expenditures:

First, Social Protection is increasing subsidies to the Household

Benefit Package and recipients of the National Fuel Allowance scheme �to

offset the cost of their water bills�. This will cost �66 million.

Second, a water tax credit scheme is being introduced. This will cost

�40 million.

Finally, the cost of providing free water allowanced for children is �on

the books�; that is, it is counted as government expenditure.

�Social transfers in kind include such items as free travel on public

transport, fuel allowances and the child-based free allowance related to

water charges.�

�How much does this cost? The Government doesn�t say. But we can

estimate. There were approximately 1,170,000 recipients of Child

Benefit. Each one of these children should be receiving a free water

allowance of 21,000 litres per year. On the basis that this will cost

�102 per child, this brings the total cost to �119 million. But this is

just an estimate so let�s be conservative and round it down to �100

million.

When we add up these costs � Social Protection subsidies, tax relief and

free water allowances for children � it comes to �200 million. This will

�cost� the Government.

When we subtract these expenditures from the �550 million net savings to

the Government from moving Irish Water off the books, the bottom-line

savings is between �300 and �350 million. Here�s the summary table.

Water Deficit

So the Government claims removing water charges will cost �800 million.

But when we factor in the lost revenue (commercial water charges) and

additional expenditure (Social Protection subsidies and tax cuts), the

net cost will less than half that: between �300 and �350 million.

Why is this so important? Because it shows that if water charges were

removed, the impact to the deficit would be miniscule (0.16 percent of

GDP). This would still leave the Government well below the deficit

target. The Government is refusing to listen to people not because it

would undermine their deficit target but because . . . well, you supply

the answer.

The Government can claim its numbers are right � but only if they ignore

the losses and additional expenditure. This is highly misleading. They

do not refer to net costs; they do not refer to the net impact on the

deficit. This is no way to debate public finances.

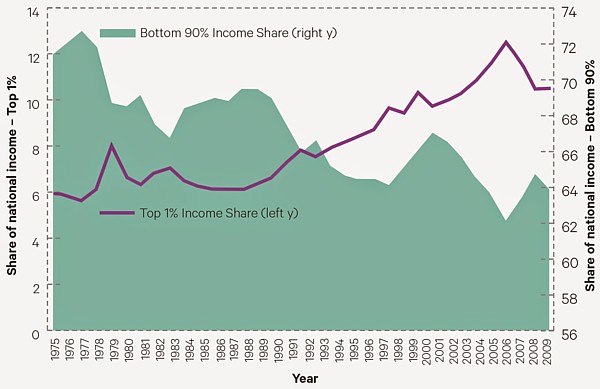

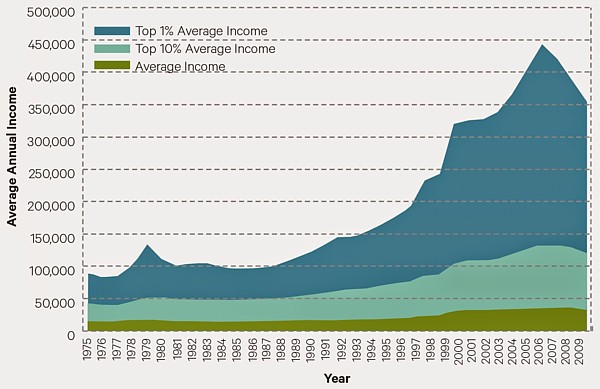

Why �gross� income inequality matters

Cormac Staunton

Gross income inequality is the

inequality of incomes from the market - including wages, self-employed

incomes and investments. When we look these incomes in Ireland over a

period of time we see a growing concentration of income in the Top 10%,

and in particular the Top 1%.

During the period of economic growth from

the early 1990s, the share of income earned by the Top 10% in Ireland

rose, meaning that the vast majority of people, the �Bottom 90%� of the

population, lost a proportional share of the national income. The Bottom

90% share of national income fell from 71.4% in 1975 to 63.9% in 2009.

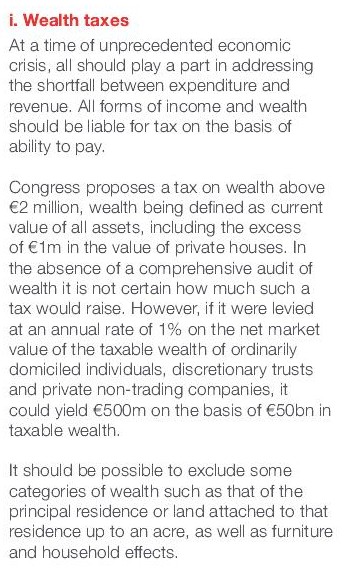

'wealth being defined as current value of all assets'

*********

Irish Statute Book

Wealth Tax Act, 1975 '�private non-trading company� means a company whose income in the

twelve months preceding the valuation date consisted wholly or mainly of

investment income'

A NEW LEVY on the wealthy

and minimum taxes for high earners are among the

measures called for in a pre-Budget submission from the

Irish Congress of Trade Unions.

An annual one per cent tax

on all wealth above �2million � including the value of

houses above �1million � could take in around

�500million a year for the State, according to the

document.

Claiming Our Future has

outlined a menu of proposals to generate badly needed

revenue to protect mid to low incomes, minimise cuts to

public services and create jobs.

These include:

a) a levy on assets and property worth over �1 million

b) high net worth Irish citizens paying their dues here

so that the number of tax exiles decreases

c) eliminating tax breaks for those with high incomes so

that they pay their fair share

d) a levy on financial transactions over significant

amounts (known as a Tobin tax) and

e) a higher tax rate on incomes over �100,000.

The revenue to be generated

from a wealth tax on assets worth over �1 million could

generate between �500 and �600 million alone per annum.

Tax expenditures in the main benefit the highest paid.

80 per cent of pension reliefs go to the top 20 per

cent of earners.

Property-related tax expenditures also disproportionably

benefit the most well off.

Tax expenditures like these effectively mean average and

low earners subsidise high earners. Changes in tax

expenditures in the area of pensions and property

related reliefs could save the exchequer in the region

of �1billion.

Minister Noonan said that between �52 million and �312

million a year could be brought in each year with a higher income tax

rate of between 42 per cent and 47 per cent for people earning over

�100,000.

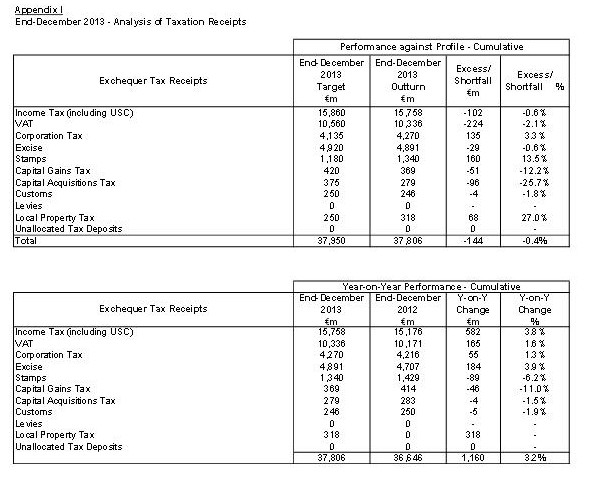

Local Property Tax brought in �318 million

in 2013.

**********

Corporation Tax

Corporation Tax for

Accounting Period 2008 in �million:

The Revenue is notified of

trading profits of �65 billion. Yet it only receives a

mere �3.9 billion in tax. This represents an effective

tax rate of six percent. In other words, companies pay

less than half the official tax rate.

Poorest 10% of households

pay higher proportion of income in tax than richest 10%

New research on the total

amount of tax Irish people pay finds that the poorest

10% of households pay a larger share of their income in

tax than the richest 10%.

When income tax and indirect taxes such as VAT are

included in the calculations the study conducted by the

Nevin Economic Research Institute finds that:

The poorest 10% of

households pay just over 30% of their income in taxes -

mostly in the form of indirect taxes levied on the

things they spend money on.

The richest 10% spend 29.5%

of their income on tax - mostly in the form of direct

income tax.

The combined tax burden

produces a u-shaped graph, with the bottom and top of

the income distribution paying most, and those on lower

middle incomes paying least.

The research was conducted

by Dr Miche�l Collins, a former member of the Commission

on Taxation. It highlights the importance of Government

thinking more broadly when considering changes to

taxation. The whole system needs to be addressed when

changes are being made, not just the income tax system.

So what about our own home-grown 1 percent?

How much wealth do they own � wealth that translates

into economic and political power? The Credit Suisse�s

Global Wealth Data Handbook 2011

(not yet available

free on-line) can give us an insight � as they estimate

the concentration of wealth holdings in the top percent

deciles.

Irish concentration of

wealth is one of the highest in the EU-15. 28 percent

of all wealth � housing and financial wealth � is owned

by the top 1 percent of adults. That�s a lot wealth for

a handful of people.

While Credit Suisse uses US

$ in their tables, we can take their proportions to

estimate how much this means in Euros and cents. They

estimate that financial wealth makes up 47 percent of

all wealth.

Using CSO data, we therefore find the following:

The Top 1 percent is made up

of approximately 36,000 adults.

This group owns

approximately �130.2 billion.

�130.2 billion. Just take a

moment to reflect on that.

[Pause for quiet

reflection on the amount of wealth owned by 36,000

adults in Ireland]

On average, this means

that every adult in the top 1 percent owns �3.8 million.

The state operated a wealth tax from 1975.

However while the initial legislation was quite strong, the Fine Gael Labour government of the day bowed to pressure and included a large

number of exemptions in the final act.

As a result the yield was low. The legislation was repealed in 1978.

The ESRI study produced a detailed research paper into the design and

operation of the wealth tax in 1985. The

report said that, �Opponents of the Wealth Tax argued that it had

detrimental effects especially on investment,

but there is no convincing evidence to support this contention.�

However the study also concluded that the cost of administering the tax

was �exceptionally high�. The most

effective way to avoid this key concern of the ESRI report is to make

any wealth tax self-assessed.

What Assets Are Included? � All income and savings � Stocks and shares and all other financial products in public companies � Shares in private non-trading companies � Land � Buildings � Second and subsequent homes including holiday homes � Personal possessions including art, cars, boats, planes, jewellery,

gold

How much would Sinn F�in�s wealth tax

raise?

In a D�il debate in 2011, Minister for Finance Michael Noonan estimated

that a French-type wealth

tax implemented here would raise between �400million and �500million in

a full tax year. Since then

the French government has strengthened the legislation underpinning

their wealth tax and expect

the annual yield to double. Based on data from the Central Bank, the CSO and Capgemini World Wealth

Report, Sinn F�in has

estimated that a wealth tax could bring in up to 0.5% of GDP or

�800 million in a full tax year.

Moving the Faberge egg

abroad is why wealth tax won't work

A levy on the super rich

often only scares away the people who create jobs and

wealth

Here in Ireland, Sinn

Fein has often called for a tax on the super rich and

Francois Hollande has introduced one in France creating

tax exiles out of well-known French citizens such as

Gerard Depardieu, members of the Peugeot family or

Chanel's owners.

Earlier this year, the Bundesbank and the International

Monetary Fund joined the fray when they both called for

some sort of one-off wealth tax in countries, like

Ireland, which effectively went bust. Indeed, in the

Cyprus bailout there really was a one-off tax on anybody

with substantial bank savings; a precedent likely to be

repeated in future bailouts.

Capital in the Twenty-First Century, the unexpected US

bestseller by Thomas Piketty is only the latest in a

long line of economic tracts to offer some sort of

intellectual argument underpinning wealth tax.

In the last century, wealth taxes were also popular with

economists as varied as Joseph Schumpeter and John

Maynard Keynes although the latter changed his mind in

later life.

Ireland's top tax rate just 'nonsense',

says Piketty Nobel-tipped economist argues for redrawing tax based on 'real' wealth

His solution is steeply rising taxes on wealth and high

incomes. The top rate on earnings above �2m a year could reach 80 per

cent, with different high rates at �500,000 and �1m a year.

He blames low tax rates � he includes the 52 per cent rate in Ireland �

for the explosion in top salaries for bankers and senior executives.

"If you're paying 50 per cent, it is well worth getting a �1m pay rise.

If 80 per cent is going to go on tax, it changes the whole situation. "That was the ratio in Britain when it had taxes of this level in the

Sixties. The USA also did it in the Thirties, although continental

European countries never went that high. "The extraordinary thing from my data is that the share of wealth

belonging to the top 10 per cent in France is the same as it was before

the Revolution. It is as if the ancien regime had never come to an end."

But he is shocked that the Irish top rate kicks in at below-average

earnings. "That is nonsense. You have to be very careful about the marginal rate

that you apply to particular incomes," he said.

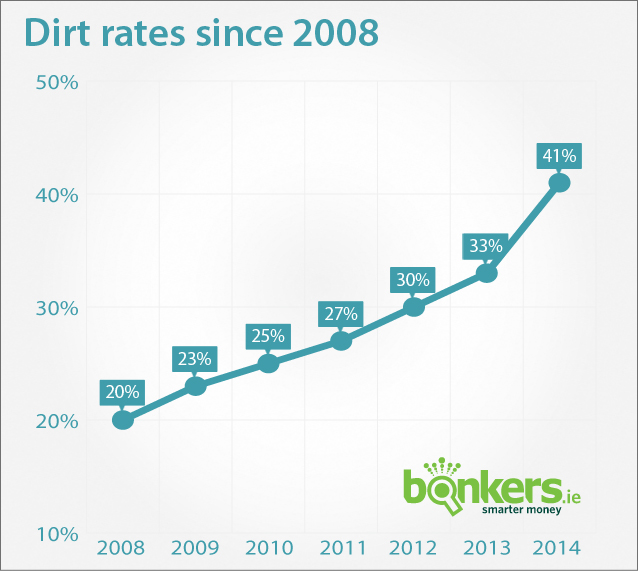

"Deposit interest retention tax

(DIRT) is a form of tax on interest earned on bank accounts in Republic

of Ireland that was first introduced in the 1980s. In Ireland, income

from any source is reckonable for taxation purposes.

The Revenue Commissioners believed that the

large majority of interest earners were declining to report it and that

the most efficient method to collect at least the basic rate tax would

be to deduct it at source. After PAYE, it was Ireland's second

experience of a withholding tax.

DIRT is deducted at source by financial institutions. The rate of

DIRT (since Jan. 2013) is 33% up until the 2014 budget which it now

stands at 41%, except where interest cannot be calculated at least

annually and cannot be determined until it is paid, in which case it is

36%."

"Deposit Interest Retention Tax (D.I.R.T.), at the rate of 33% (from the

1st January 2013) is deducted at source by deposit takers (e.g. banks,

building societies, Credit Unions, Post Office Savings Bank, etc.) from

interest paid or credited on deposits of Irish residents.

The above D.I.R.T. rate was:

30% for the period 1st January 2012

to the 31st December 2012

27% for the period 1st January 2011 to the 31st December 2011

25% for the period 8th April 2009 to the 31st December 2010

23% for the period 1st January 2009 to the 7th April 2009 and

20% for the period 1st Janury 2002 to the 31st December 2008"

�DIRT� tax on savings interest to rise to 41 per cent

Oct 15 2013

"The measure means those saving money will have to hand �41 back to the

state for every �100 in interest they accrue.

FINANCE MINISTER MICHAEL Noonan has confirmed an increase in the rate of

annual DIRT tax applied to savings interest, from 33 per cent to 41 per

cent.

It means those saving money will have to hand �41 back to the state for

every �100 in interest they accrue.

Aimed at convincing people to spend money rather than sit on large sums,

the move has been criticised by accountants Grant Thornton � which says

is may encourage people to try and evade the payment:

�The DIRT tax on savings has now gone from 20 per cent to 41 per cent in

a short period of time,� partner with the firm Peter Vale said.

�Whilst the move may encourage people to stop hoarding cash and invest

in more productive assets, it also increases the likelihood of greater

non compliance in terms of returning details of interest income to

Revenue.�"

"Preliminary data from the US Bureau of

Economic Analysis (BEA) on majority-owned foreign affiliates of US firms

show that in 2010 (latest available), Irish-based firms reported net

income of $95.6bn and a payroll count of 98,500, which gives profits per

employee of $970,000.

In one recent year, the profits per

employee at US-owned companies in Ireland were at $970,000 while the

corporate tax paid in Ireland was about $25,000 (�19,000)."

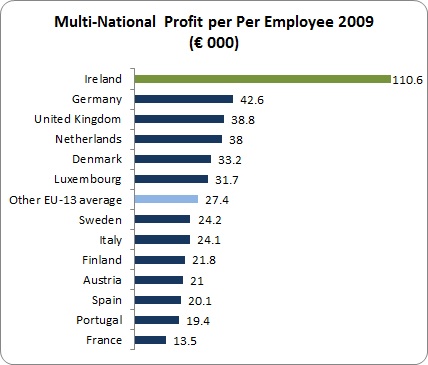

"Ireland is not just a league-leader, it

is off the chart.

MNCs here make more than four times the

profit per employee than the average of the other EU-15 countries

reporting (no data for Belgium or Greece).

No wonder more and more multi-nationals

are making Ireland their home.

It should be noted that this Eurostat

data does not include the financial sector, so the massive profits being

made in the IFSC are not included. Nor does the above include taxation."

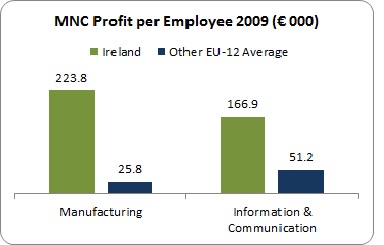

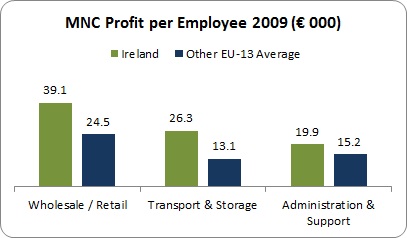

"In each of these sectors � particularly

retail and transport � MNC profits in Ireland significantly exceed the

average of other countries.

Only in two sectors � the Professional & Scientific and Accommodation �

is MNC profit in Ireland lower than the average of other EU countries.

These two sectors, however, are relatively small, making up less than

two per cent of the turnover of all MNCs in Ireland."

'Forbes names Ireland as �best country for

business�'

Colin Gleeson Thu, Dec 5, 2013,

"Article in influential US magazine says economic downturn has made

Ireland more attractive.

Ireland has for the first time been named as the �best country for

business� in rankings carried out by renowned US financial magazine

Forbes.

Ireland has moved up from sixth position in the influential rankings

last year. The rankings are determined by grading 145 nations on 11

different factors: property rights, innovation, taxes, technology,

corruption, freedom (personal, trade and monetary), red tape, investor

protection and stock market performance.

Each category is equally weighted and the data comes from published

reports from the following organisations: Freedom House, Heritage

Foundation, Property Rights Alliance, Transparency International, World

Bank and World Economic Forum.

In an article announcing the results of the rankings, Forbes describe

Ireland as having been �devastated� by the recession and in receipt of

an �85 billion bailout to prop up the banking system.

�Despite these economic troubles, Ireland still maintains an extremely

pro-business environment that has attracted investments by some of the

world�s biggest companies over the past decade,� says the magazine.

�Ireland scored well across the board when measuring its business

friendliness. It is the only nation that ranks among the top 15 per cent

of countries in every one of the 11 metrics we examined to gauge the

best countries,� says the article.

Ireland ranked �near the very top� for low tax burden, investor

protection and personal freedom.

The article quotes Moody�s Analytics� economist Melanie Bowler who

specialises on Ireland. She says Ireland has continued to attract direct

foreign investment �despite its problems�.

She highlights the �educated workforce� and 12.5 per cent corporate tax

rate as �big draws� for companies, as well as the language factor. �You

want to have a common language if you are setting up operations in

Europe,� she says.

�Dublin has already established itself as a location for multinationals,

so it has the necessary infrastructure for other companies to easily

move into the country and set up shop.�

The article in Forbes also says the State�s recent troubles have made it

�more attractive� for companies moving in.

�Nominal wages fell 17 per cent between 2008 and 2011, which helped keep

labour costs in check. Unemployment remains stubbornly high � a recent

12.8 per cent � providing companies a large labour pool to pick from.

�There are now more than 1,000 overseas companies with a presence in

Ireland and they employ 150,000 of the nation�s 1.9 million workers.�

New Zealand placed second in the rankings � down from first place last

year � while Hong Kong completed the top three.

Minister for Jobs, Enterprise and Innovation Richard Bruton said the

finding by Forbes was a testament to the hard work and innovation of

Irish businesses and workers.

Speaking from Indonesia where he is attending the World Trade

Organisation ministerial conference, he said: �It is the latest in a

range of indicators which shows that the environment for business here

is steadily improving, and shows that the hard work and sacrifices of so

many people are yielding tangible results in terms of international

competitiveness and the jobs we so badly need.�"

Current

expenditure is recurring spending or, in other words, spending on items

that are consumed and only last a limited period of time.

They are

items that are used up in the process of providing a good or service.

In the

case of the government, current expenditure would include wages and

salaries and expenditure on consumables - stationery, drugs for health

service, bandages and so on.

What is Capital Expenditure?

Capital

expenditure is spending on assets.

It is the

purchase of items that will last and will be used time and time again in

the provision of a good or service.

In the

case of the government, examples would be the building of a new

hospital, the purchase of new computer equipment or networks, building

new roads and so on.

What is Gross domestic product (GDP) ?

Gross

domestic product (GDP) is the market value of all officially recognized

final goods and services produced within a country in a given period of

time.

GDP per capita is often considered an indicator of a country's

standard of living.

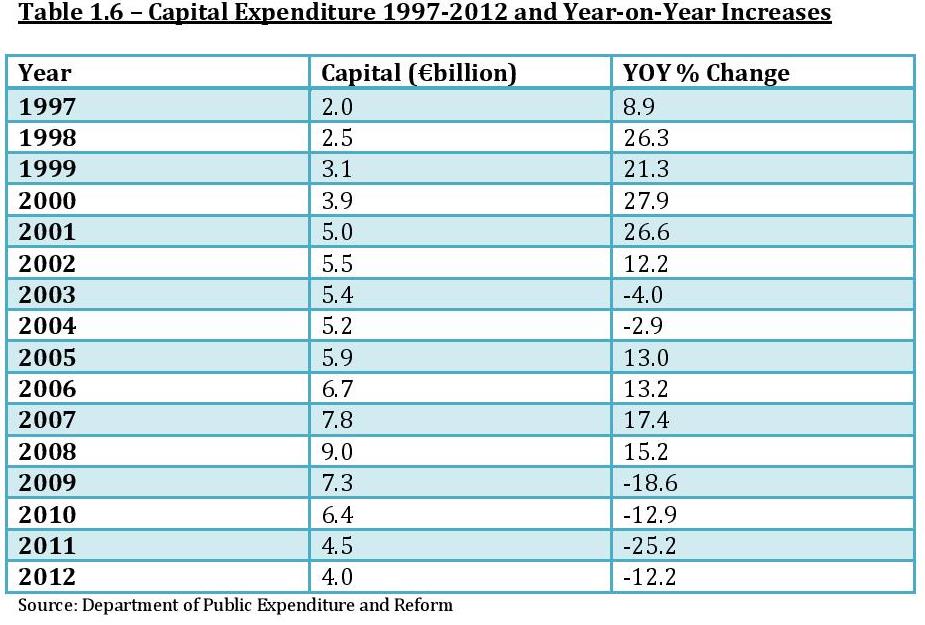

"Table 1.6 shows annual

capital expenditure by the state from 1997 to 2012.

The peak

in capital expenditure was in 2008 when �9bn was spent and

has fallen to under �4bn in 2012 representing a fall in

capital expenditure of 56%.

Capital expenditure was reduced

by a further �0.55bn in Budget 2013 and an additional �0.1bn

in savings via capital expenditure is planned for Budget

2014."

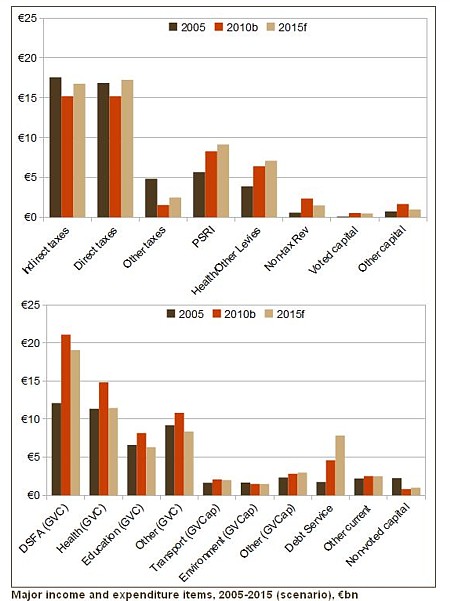

Major income and expenditure items,

2005-2015 (scenario), �bn

DSFA = spending by the Dept of Social &

Family Affairs

�GVC� refers to �Gross Voted Current� expenditure

�GVCap� refers to �Gross Voted Capital� expenditure

(All spending by the Government is either gross or net, voted or

non-voted and current or capital.)

Voted expenditure is

essentially the money allocated to government departments and offices.

Non-voted expenditure is money that is spent under specific legislation

and does not require a separate �vote�.

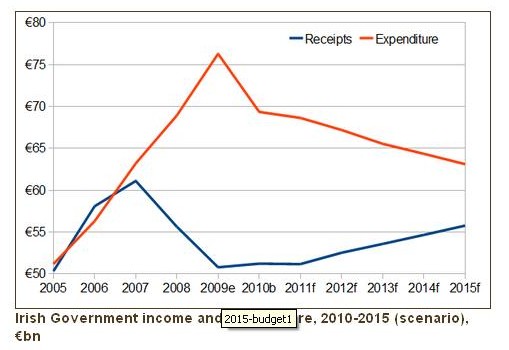

What will Ireland�s government

finances be like in 2015? A five-year view on the Budget

22 Dec 2009 [Ronan Lyons]

"What will Ireland�s government

finances look like in 2015, though? Will we be back in

Maastricht territory, with a Budget deficit of less than 3%?

What about our national debt? And how tough will the next

five Budgets be? To understand that, it�s necessary to go

right back to basics with Ireland�s finances.

For example, we all know that the Government will take in

just �34bn this year while spending over �60bn, right?

Wrong! Those figures are net figures, it turns out. To go

back to basics, we need to look at the gross figures, i.e.

count receipts such as PRSI and health levies as part of

income, as opposed to netting them off against government

expenditure. Doing that, total receipts for 2009 come to

just over �50bn, while total expenditure will top �76bn.

By coincidence, total receipts for 2005 were also just over

�50bn, giving us an appropriate year to compare ourselves

to. The distinction between gross and net turns out to be an

important one, because it reveals how the Government�s

funding sources have changed.

Whereas PRSI, other levies (such as the health levy) and

what is classed as �non-tax revenue� brought in about �10bn

in 2005, Budget 2010 estimates that these sources will bring

in over �17bn � a staggering 70% increase. (The

government�s income going up? Now, there�s a headline you

won�t read in the papers!)

Meanwhile, indirect, direct and other taxes (�other�

includes stamp duties and capital taxes) have fallen during

the same period from just under �40bn in 2005 (they actually

peaked in 2007 at �47bn) to about �32bn in 2009 and 2010.

It is in expenditure, however, where the real changes have

occurred. In 2005, instead of �69bn, total expenditure by

the Government was �51bn. To repeat, whereas the

Government�s total income next year will be the same as in

2005, expenditure will be more than one third higher.

Of the �18bn increase in spending, half has come from gross

spending on social welfare. Most of the remaning increase (a

further �7bn) has come from other current expenditure areas,

most notably health and education.

It�s worth pointing out that all the money spent on social

welfare and the vast majority of the money spent on health

and education goes in the form of someone else�s income."

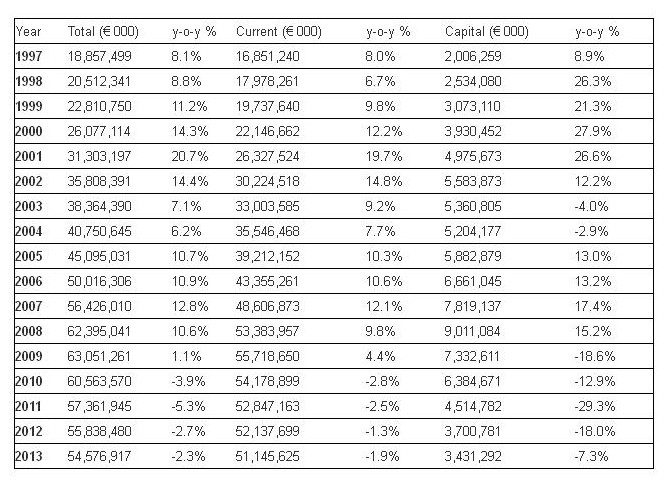

"Gross

voted public expenditure for the period 1997 to 2013 is

summarised in the table above. The figures represent all

current and capital spending by Government Departments and

some of their agencies, including spending from the Social

Insurance Fund, but does not include non-voted spending

directly from the Central Fund such as debt-servicing costs.

All figures are actual outturn figures, apart from the

figures for 2013 which are in line with the Revised

Estimates published in April 2013, and the 2012 figures

which are the provisional outturn figures as also published

in the Revised Estimates in April 2013. The year-on-year

percentage variations are also shown."

http://per.gov.ie/expenditure-trends/

Gross Public Expenditure peaked

in 2009 but has been in decline since due to cutbacks.

"Both the

Fianna F�il and Fine Gael-Labour governments have set out to

severely curb the spending of the public sector. A glance at

any of the leading newspapers or other media demonstrates

that there is an overwhelming consensus that public spending

must be cut. Implicitly, and often explicitly, an

unsustainable level of public spending is held to be the

cause of the current crisis.

That this nonsense has such traction in the public debate

tells us more about the society in which that debate is

being conducted than about the economy itself. Prior to the

crisis, the level of public spending was 36.7 per cent of

GDP in 2007, nearly 10 percentage points lower than the euro

area average of 46 per cent."

http://www.theirelandinstitute.com/citizen/c04-burke-print.html

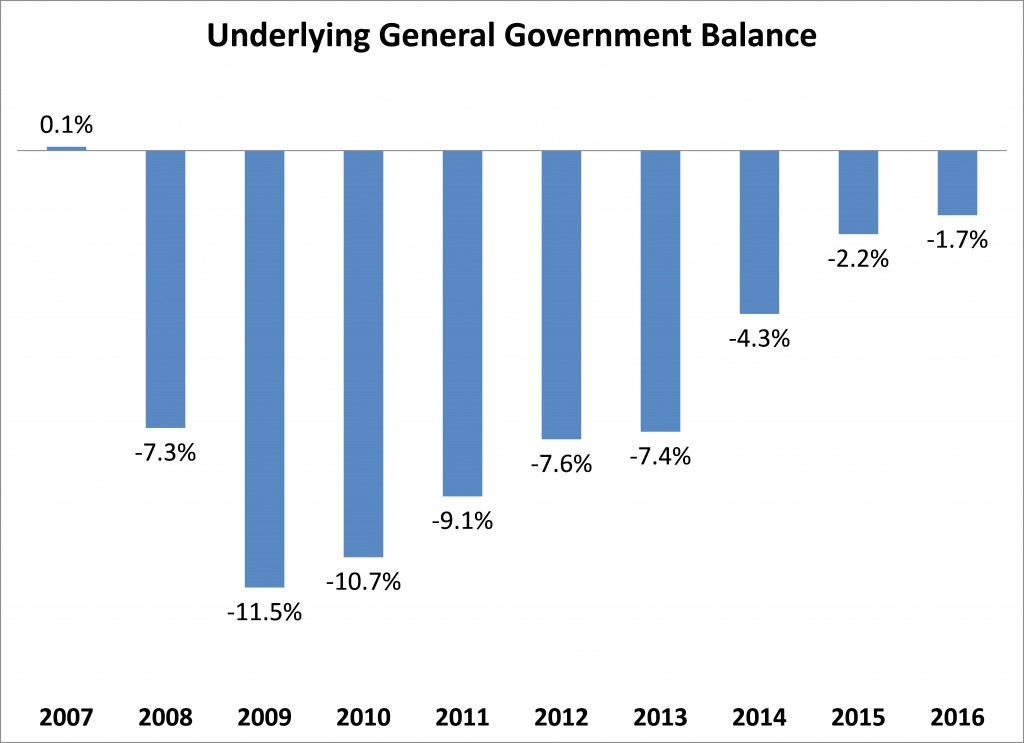

"Since 2008, the public finances have come

under increased strain due to a collapse of tax revenues and an increase

in expenditure on social transfers and debt servicing costs.

Table 1.7

depicts the deterioration of the underlying General Government Balance

(i.e. excluding once-off bank recapitalisation costs) from a small

surplus in 2007 to a large deficit of -11.5% in 2009."

http://www.publicpolicy.ie/irelands-current-fiscal-profile/

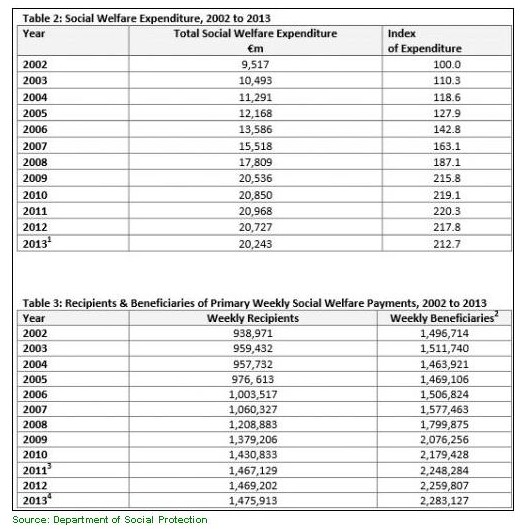

'Irish Budget 2014: Half of Ireland's

population on welfare'

By Michael Hennigan

Sep 2, 2013

"Half of Ireland's population is on welfare and when recipients of child

benefit, farmers dependent on public subsidies which are effectively

welfare, accounting for 81% of average farm income in 2012; legal

services costing the state about a half billion euros annually; public

payments to doctors; a raft of corporate welfare schemes and the public

service itself, [...] in Ireland there is a shining example of the

halfway house known as [...] dependency on the State.

This year, the Department of Social Protection will spend over �20.24bn

on its entire range of schemes, services, and administration. At the end

of May, there were 1.476m people receiving a weekly payment in respect

of 2.283m beneficiaries. In addition, some 614,000 families were in

receipt of the monthly child benefit payment.

The CSO estimated that the total population was at 4.593m in April

2013."

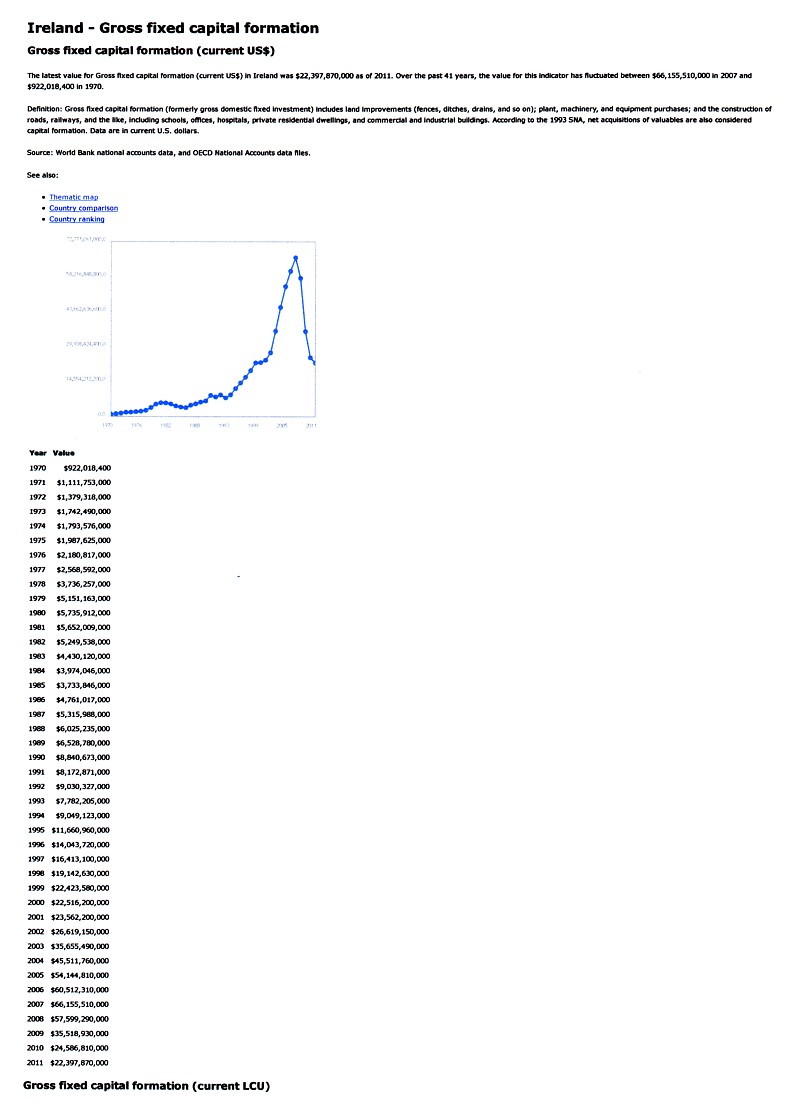

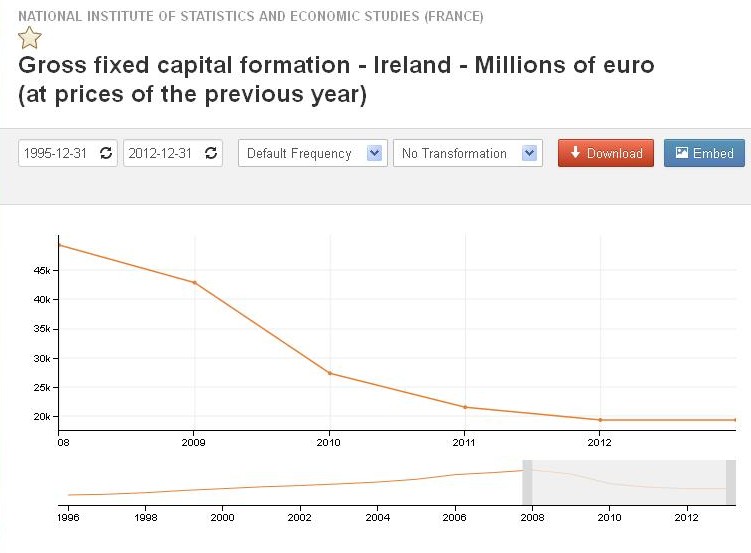

Gross fixed capital formation

(formerly gross domestic fixed investment) includes land improvements

(fences, ditches, drains, and so on); plant, machinery, and equipment

purchases; and the construction of roads, railways, and the like,

including schools, offices, hospitals, private residential dwellings,

and commercial and industrial buildings.

"Ireland�s budget deficit for 2012 has been revised upwards from �12.5bn

to just over �13.5bn making it the third largest in the EU.

The new figure means that the deficit represented 8.2% of GDP rather

than the 7.6% estimated back in April. According to the CSO, the

revision arose mainly from Government revenue from mobile phone licence

sales being initially recorded for 2012, rather than for 2013.

While the 8.2% figure is higher than first anticipated, it is still a

vast improvement on the 2011 deficit of �21.36bn; which amounted to

13.1% of GDP. Furthermore, it was still better than the 8.6% of GDP

target set by the troika for 2012.

Final annual data, published yesterday by Eurostat, the EU�s statistical

agency, showed only Spain and Greece as having a higher budget deficit

than Ireland last year. While Spain�s jumped from 9.6% of GDP to 10.6%;

Greece�s actually lowered from 9.5% in 2011 to 9% for last year.

While 15 member states saw their deficits improve last year, one

remained stable and 12 saw a worsening. Sweden, Estonia, Luxembourg and

Bulgaria had the lowest deficits � ranging from 0.2% of GDP to 0.8%.

Britain recorded a deficit of 6.1% of GDP; down from 7.7% in 2011.

Germany, meanwhile, was the only EU nation to deliver a government

surplus. Seventeen member states had deficits higher than 3% of GDP.

Eurostat also noted that as of the end of 2012, the lowest ratios of

government debt to GDP were recorded in Estonia, Bulgaria, Luxembourg

and Romania; with the highest observed in Greece, Italy, Portugal and

Ireland (117.4%, up from 104.1% in 2011). The eurozone�s deficit stood

at 3.7% of GDP, with the EU, as a whole, 3.9%.

The Government�s official deficit target, for 2013, has been set at 7.4%

of GDP, with some commentators suggesting it should marginally beat

that.

�Ireland�s strategy in the past couple of years has been to

under-promise and over-deliver on its budgetary targets, a trend that we

believe is likely to be maintained in 2013. Despite the fact that the

risks to the Government�s economic growth projections are clearly to the

downside at this juncture, we still think that come end-December the

budget deficit out-turn as a percentage of GDP will once more be lower

than the 7.4% figure officially targeted, as the Department of Finance

has allowed itself plenty of leeway. Our forecast is for a marginally

lower figure of 7.3%,� said Alan McQuaid of Merrion Stockbrokers."

"The Dept [of Finance] is forecasting

a general government budget deficit of �12.65 billion in 2013, or 7.5%

of GDP, below the expected budget deficit of �13.3 billion or 8.2% of

GDP for 2012. The decline in the budget deficit would be more pronounced

in 2013 but for the fact that sizeable interest payments totalling

almost �2 billion begin to fall due on the Promissory Note Programme.

This will boost the budget deficit by 1.1% in 2013.

In its Medium Term Fiscal Statement published last month, the government

projected that over �5 billion of further fiscal consolidation measures

will be required in 2014 and 2015 to reduce the budget deficit to under

3% of GDP by 2015. These will consist of additional spending cuts of

some �3.3 billion and tax increases of �1.8 billion."

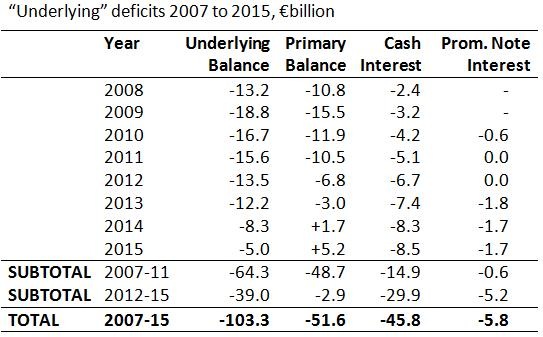

the underlying balance in 2012 is -13.5bn. If

�underlying deficits�

(deficits excluding direct payments to banks) then the difference

between -19.18bn and

-13.5bn = -5.68bn, then presumably 5.68bn

was given to the banks.

If the -13.5bn 'underlying' deficit in 2012 was made up of -6.8bn

[Primary Balance] and -6.7bn [Cash Interest] then we can see that

interest repayments grew to become 50% of the deficit compared to 2008

when the Primary Balance was -10.8bn and the Cash Interest -2.4bn.

In other

words, as we borrow money to cover the deficit, then a larger and larger

percentage is being borrowed just to pay the interest on the debt.

If we look at the deficit figures projected for 2014

we can see that all the money to be borrowed, 8.3bn, is to be spent on

interest repayments.

In 2015 it is projected that all the money

borrowed, 5bn, will pay for some of the interest repayments with tax

revenue covering the rest.

A promissory note is a legal instrument (more particularly,

a financial instrument), in which one party (the maker or

issuer) promises in writing to pay a determinate sum of

money to the other (the payee), either at a fixed or

determinable future time or on demand of the payee, under

specific terms.

The Irish Times

Oct 10, 2013

'Promissory note law

could involve �limitless� public monies'

Note in favour of EBS provides

Minister can adjust sum paid upwards or downwards, court

told

"The Minister for Finance used powers under a 2008

�emergency� law to create a promissory note in 2010 which

can be adjusted to allow for the payment of �possibly

limitless� amounts of public monies, the High Court was told

today.

John Rogers SC said the promissory note issued in favour of

the Educational Building Society, under which �250 million

was paid to the Society earlier this year, provides the

Minister can adjust the sum to be paid either upwards or

downwards and permits the creation of �very significant,

possibly limitless� liabilities for the taxpayer.

The sums involved were certainly not predictable when the

note was created in June 2010, he added.

Mr Rogers was continuing his arguments on behalf of United

Left TD Joan Collins in the continuing hearing of her

challenge to the making of promissory notes in 2010 in

favour of Anglo Irish Bank, EBS and Irish Nationwide

Building Society as part of the �31 billion capitalisation

of those institutions.

Ms Collins argues the making of the notes, under the

provisions of the Credit Institutions Financial

Stabilisation Act 2008, which he said appeared to have been

�emergency� legislation, was unlawful because it involved

the Minister appropriating public monies for expenditure

when, under the Constitution, such �appropriation� was

solely a matter for the D�il.

The State denies the claims and argues the TD�s case is

based on a fundamental misunderstanding of the relevant

constitutional provisions.

The court has heard, following the liquidation of Irish Bank

Resolution Corporation (formerly Anglo) last February, that

the �25 billion promissory note issued to that bank was

exchanged for Government bonds due to mature after periods

of between 25 and 40 years.

Mr Rogers argued today, given his side�s claim the

promissory notes are illegal, those bonds cannot be valid.

Because the action raises important constitutional issues

with implications for the entire basis of the State�s

funding, it is being heard by a three-judge court comprising

Mr Justice Peter Kelly, Ms Justice Mary Finlay Geoghegan and

Mr Justice Gerard Hogan.

A government bond is a bond issued by a

national government, generally with a promise to pay periodic interest

payments and to repay the face value on the maturity date.

Government bonds are usually denominated in

the country's own currency.

Bonds issued by national governments in

foreign currencies are normally referred to as sovereign bonds, although

the term "sovereign bond" may also refer to bonds issued in a country's

own currency.

The terms on which a government can sell bonds depend on how

creditworthy the market considers it to be. International credit rating

agencies will provide ratings for the bonds, but market participants

will make up their own minds about this.

Treasury Bond

Issue Date

Maturity Date Coupon Date

ISIN Code

4.6% 2016

11 May 1999 18 Apr. 2016

18 Apr.

IE0006857530

OFFERING CIRCULAR

National Treasury Management Agency

4.60% Treasury Bond 2016

Issue to take place on 11th May, 1999

See Overleaf for Conditions

ISIN Code: IE0006857530

National Treasury Management Agency

10th May, 1999

OFFERING CIRCULAR

CONDITIONS ATTACHED TO THE 4.60% TREASURY BOND 2016

The principal and interest of the above bond, which is

issued under the authority of the Finance Act, 1970 and

other statutes, will be charged on the Central Fund.

Purpose of Issue: The proceeds of the issue will be used

for general financing purposes of the Exchequer.

Trustee Status: The bond is an authorised trustee investment

and trustees may invest in the bond even if the price at

time of investment exceeds the redemption value of �100 per

cent.

Taxation: Interest on the bond will be paid gross without

deduction of income tax or any other deductions or

withholdings.

In general, where the holder of the bond is an Irish

resident taxpayer, the interest element payable on the bond

is assessable to income tax, whereas any gains arising on

disposal of the bond are exempt from capital gains tax.

However, where the bond holder resident in Ireland is

dealing in Government bonds as part of a trade, he/she is

assessable to income tax or corporation tax, as the case may

be, in respect of the interest element and also the gains

arising on disposal or on redemption of the bond.

Section 43 of the Taxes Consolidation Act, 1997 provides

that the bond and the interest payable thereon is exempt

from all Irish taxation so long as it is shown that the bond

is in the beneficial ownership of a person not ordinarily

resident in Ireland. However, where the bond is held by or

for an Irish branch or agency of a foreign financial

concern, interest and gains on such stock will be chargeable

to tax.

Individual purchasers should note that, where the bond is

the subject of a gift or inheritance, the conditions for

exemption set out in Section 57 of the Capital Acquisitions

Tax Act, 1976, as amended by Section 40 of the Finance Act,

1978 are met.

In addition, the execution of instruments for the issue and

the transfer of the bond will be free of Irish stamp duty.

Interest: Interest on the bond will be paid annually on 18th

April. The first interest payment will be made on 18th

April, 2000 and be at a rate of 4.2732%. Interest payable

will be calculated in accordance with the �actual / actual�

day count convention.

The interest payable on each interest payment date will be

based on the balance in the account (s) on the register

maintained by the Central Bank of Ireland, as at close of

business on the preceding business day.

Principal: The principal of the bond will be repaid at par

on 18th April, 2016.

Account: It is a condition of this bond that registered

holder(s) shall nominate an account in a credit institution

linked to the European System of Central Banks� Payment

System (TARGET) into which all dividend/redemption payments

will be made. Details of the account to which such payments

are to be made must be provided to the Central Bank of

Ireland (as Registrar) on the appropriate form, which is

available from the Bank, by close of business (5.00pm) on

the day of registration of the holding. Holders must notify

the Registrar of any change in account details through

completion and lodgment of a further copy of the form.

Registration and Transfer: The register of holders of this

bond issue will be kept at the Central Bank of Ireland.

Stock Certificates shall not be issued. Transfer of

ownership will be evidenced by book entry in the register of

holders held by the Registrar in any sums which are

multiples of one cent.

Stock Exchange Listing: The bond will be officially listed

on the Irish Stock Exchange.

What is an ISIN? An International Securities Identification Number (ISIN)

uniquely identifies a security. Its structure is defined in

ISO 6166. Securities for which ISINs are issued include

bonds, commercial paper, stocks and warrants. The ISIN code

is a 12-character alpha-numerical code that does not contain

information characterizing financial instruments but serves

for uniform identification of a security at trading and

settlement.

http://en.wikipedia.org/wiki/International_Securities_Identification_Number

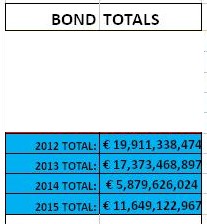

Thursday, 27 December 2012

THE DIRTY DOZEN w/e Dec 30th 2012

"Final week of 2012 and boy, was it a good year to be bondholder in

an Irish bank. The last of the �20+ billion will be paid out this

Friday, Dec 28th, a bond of nearly �40 million, unsecured, from Bank of

Ireland - more very happy failed punters cashing in at our expense. I

wonder, whatever happened to that much trumpeted separation of bank and

sovereign debt agreed to last June?

Anyway, Happy New Year to you all, though that much is already

guaranteed for those whose bonds 'mature' in 2013, �17bn in total in

2013. Add that to the �9bn in government bonds that fall due in 2013,

throw in the projected budget deficit of �14.5bn and lads - we'd better

get down to work. That's a hell of a lot of additional debt on top of

the debt we already have, don't ye think?"

'AIB repays �1 billion to unsecured

bondholders today'

More than �18 billion has been repaid

to bondholders by state-owned Irish banks this year.

"BAILED-OUT ALLIED Irish Banks (AIB) will

today repay �1 billion in unsecured debt to senior bondholders.

In a move effectively financed by the State, the money will bring to

more than �18 billion the amount that Irish banks have repaid to

bondholders this year as a result of the bank guarantee introduced in

2008.

It is the last payment that is due to AIB, which is 99.8 per cent owned

by the State, this year but there will be a number of other payments

made to unsecured bondholders in State-0wned banks before the end of the

year.

Another �2 billion is due to bondholders before the end of the year in

Anglo Irish Bank, Bank of Ireland, EBS building society, and Irish Life

and Permanent. A further �17 billion will be handed over next year.

Protesters from Sinn F�in and the Campaign against Household and Water

Taxes are due to demonstrate against the bond repayment in Dublin later

today.

Independent TD Stephen Donnelly, who has been heavily critical of

bondholder repayments, has been handing out �1 billion notes at Dart

stations in Dublin today in a bid to highlight the issue.

The notes, which were produced in conjunction graphic designer Con

Kennedy, feature Finance Minister Michael Noonan on the front and a

brief note explaining what is happening on the back."

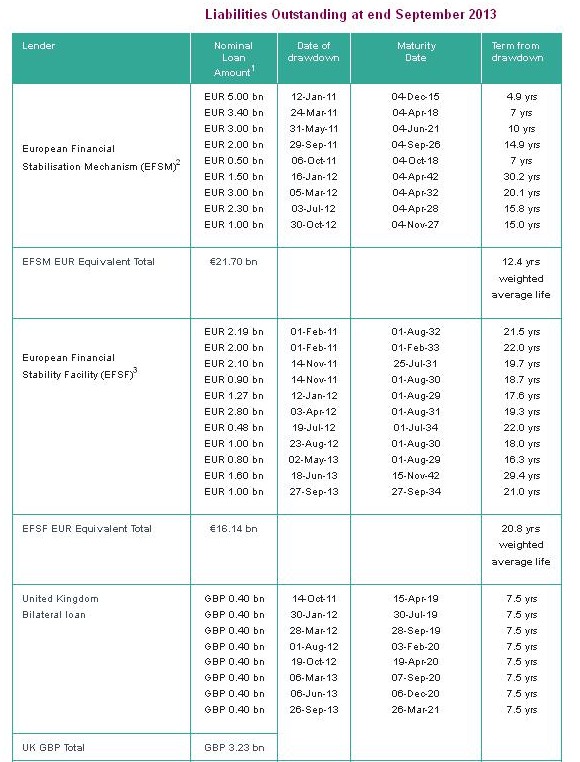

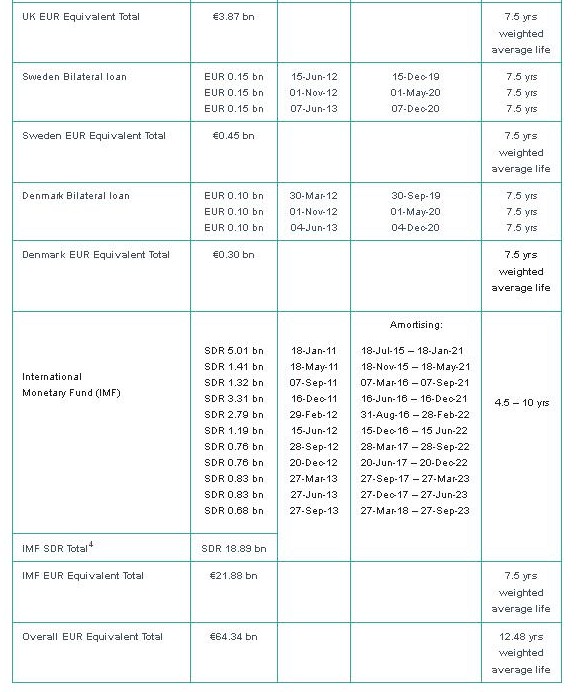

"The Government agreed, on 28 November

2010, to a three-year �85 billion financial support programme for

Ireland by the EU and IMF. The State�s contribution to the programme

will be �17.5 billion while the external support will amount to �67.5

billion.

The external support under the programme comprises:

�22.5 billion from the IMF Extended Fund Facility;

�22.5 billion from the European Financial Stabilisation Mechanism; and

�22.5 billion from the European Financial Stability Facility (�17.7bn)

and bilateral loans from the United Kingdom (�3.8bn), Sweden (�0.6bn)

and Denmark (�0.4bn)."

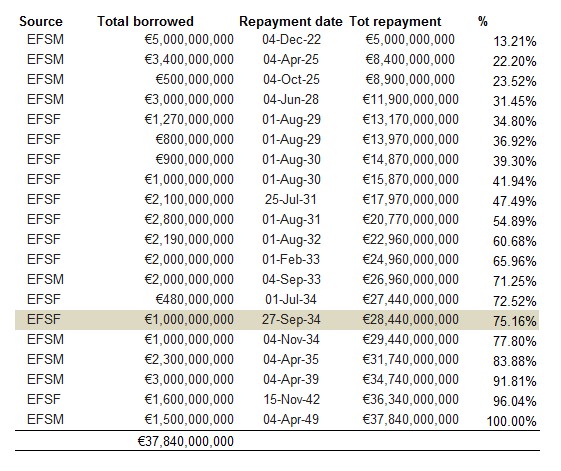

The Irish people will be paying back EU

loans until 2042 and IMF loans until 2023

'What

the IMF � EU Bailout for Ireland means in detail!'

"The facility will be made up as follows:

�35 billion to support the banking system;

�10 billion for the immediate recapitalisation and

�25 billion will be provided on a contingency basis.

�50 billion will be provided to cover the financing of the State."

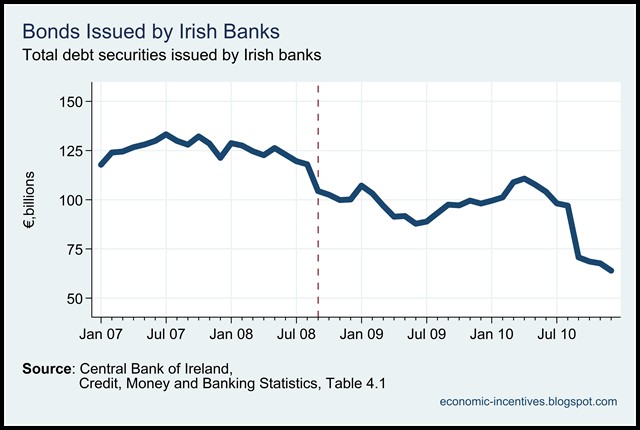

"Prior to the guarantee in September

2008 the quantity of bonds was beginning to decline. This continued up

until the summer of 2009 after which there was a stabilisation, and even

a slight increase, in the bonds in issue.

By April 2010 there was �111 billion of

bank bonds (actually �6 billion more than in September 2008), but by the

end of 2010 this had fallen to �64 billion � a drop of over �47

billion. Most of this money was fully repaid."

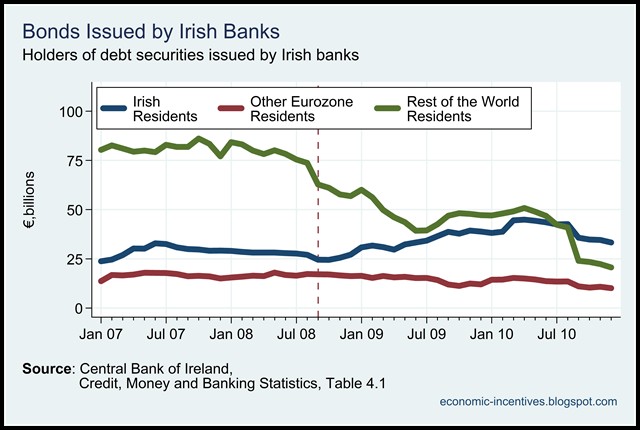

"So who got the money? The Central Bank

breaks the total down by Irish, Other Eurozone and Rest of the World

residents.

The biggest drop has occurred for

bondholders from the rest of the world which stood at �74 billion in

August 2008 and has dropped (or been repaid) by such an extent since the

guarantee was introduced that it is now down to �20 billion.

A drop of �54 billion since August 2008.

As late as last August there were �41 billion of bonds held by rest of

the world residents but there was a reduction of �17 billion in

September."

"Irish residents have seen their

holdings of Irish bank bonds rise from �25 billion at the time of the

guarantee to �45 billion in April 2010.

Since then, these too have fallen and

were down to �33 billion by December [2010].

The proportion of bond held by Irish

residents has been rising since the guarantee was introduced and now

stands at just over 50%. Are we going to burn ourselves?

Since the guarantee holdings of Irish

bank bonds by other Eurozone residents has fallen from �17 billion to

�10 billion. This would hardly leave a ripple on the European banking

system.

This would similarly apply to the �20.5

billion held by residents of the rest of the world. Non-payment of the

�33 billion owed to Irish residents would be far more significant."

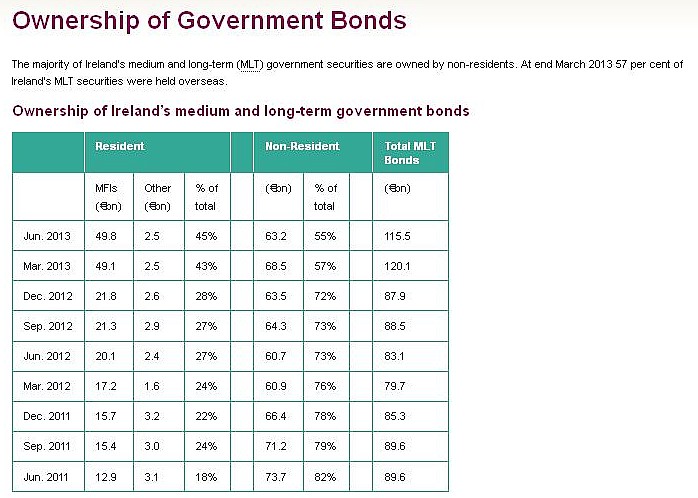

Domestic ownership of Irish

government bonds rises from 28% to 48% since 2012

By Finfacts Team

Aug 13, 2014 - 3:01 PM

The domestic ownership of Irish government bonds rose from 28% at end

2012 to 48% in June 2014 and the biggest factor was the Central Bank's

2013 deal on the promissory note debt of ex-Anglo Irish Bank (renamed

IBRC) -- see NTMA profile here - - the 2013 IBRC Promissory Note

repayment (non-cash settlement) resulted in �25bn of long-dated

Government bonds being issued to the Central Bank of Ireland on

liquidation of IBRC.

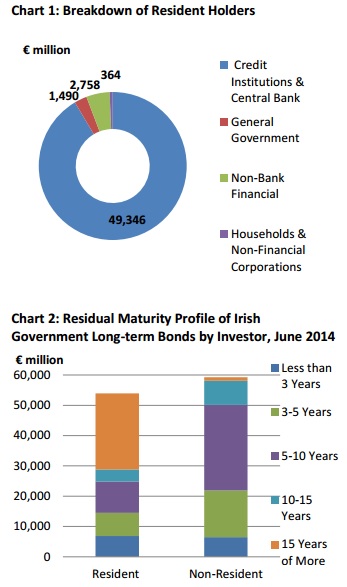

The Central Bank said today that outstanding government bonds stood at

�113.21bn in June 2014, with 11% due to mature in less than three years.

At end-June 2014, resident holders held 47.7% of long-term Irish

government bonds. resident credit institutions and the Central Bank of

Ireland, account for 91% of resident holdings.

At the end of 1999, over 70% of Irish bonds were held by domestic

investors with the balance in the hands of overseas investors. At end

2011 78% of Ireland�s MLT securities were held overseas according to the

NTMA - the debt agency.

The resident non-bank financial sector reported holdings of �2.76bn in

June 2014. The holders within this sector were predominately other

financial intermediaries at �1.13bn (Chart 1).

32% of outstanding Government bonds will mature within the next 5 years.

27% of resident holders fall under this maturity category, while the

equivalent ratio for non-resident holders is higher at 37%. Furthermore,

30% (or �17.7bn) of long-term bonds held by non-resident investors will

mature from 2023 onwards (Chart 2).

'Noonan to meet Troika after Budget to discuss

bailout exit'

12 October 2013

"FINANCE Minister Michael Noonan has hinted that

Ireland might not have to apply for a precautionary credit line when it

exits the bailout.

The Government has already indicated it might look for a �10bn credit

buffer to guard against market shocks.

But Mr Noonan told the Fine Gael national conference the National

Treasury Management Agency (NTMA) has built a �25bn fund which can act

as a significant buffer after Ireland exits the bailout.

"If we never borrowed another bob, we're cash-funded into 2015," Mr

Noonan said.

He was echoing similar comments made by EU economics commissioner Olli

Rehn this week, who said Ireland might be able to exit the bailout

without a �precautionary arrangement�.

Mr Noonan said he will start consulting with the Troika after the Budget

on how to manage Ireland�s exit from the bailout.

�Countries who have exited IMF Programmes have had follow up programmes

or backstop arrangements to ensure a return to the markets at very

little risk,� he said.

�Ireland is fortunate that the NTMA has almost �25 billion in cash

balances as we return to the market so we have a backstop already in

place."

"The National Treasury Management Agency (NTMA) is

presently sitting on a cash mountain of nearly �25bn. It places it on

deposit in the Central Bank of Ireland and receives interest at a rate

of just 0.1% per annum � yes, just zero point one per cent! The �25bn is

either borrowed or could be used to pay down borrowings which cost us an

average of 3.5% per annum. In other words, this State is sitting on a

cash mountain costing us �875m a year in interest and if you deduct the

�25m we get from the Central Bank, in net terms this mountain of cash is

costing is �850m! Per Year!

Now, there is a reason why the NTMA does keep a cash reserve. Ireland is

in a precarious financial position with a general government deficit

over �10bn per annum and our deficit: GDP was about 8% in 2012 which is

horrendous. And at the end of 2013, the funding from the �67.5bn

external bailout from the so-called Troika comes to an end. And we have

colossal borrowings which we need to repay � previously issued bonds and

repayments to the Troika.

So the NTMA calculates that it needs some reserve or buffer. It

calculates that if markets know there isn�t such a buffer, then those

markets will demand higher rates of interest than they otherwise would

on new issuance of bonds. Which all seems rational.

So, we�re buying insurance for the funding of the State which is costing

us �850m per annum."

"The State's debts are already intimidating, approaching

�200bn gross, with the risk of further liabilities emerging in the banks

and huge unfunded pension liabilities. It is easy to forget that the

State owns some financial assets too, mainly a large pile of cash (about

�25bn) resting in the accounts of the Exchequer.

The cash, on deposit at tiny interest rates, arises because the

government borrows in advance of actual requirements. The cash pile is

surprisingly large right now, reflecting bond issues by the National

Treasury Management Agency, which pays market interest rates when it

borrows but earns substantially less on the funds deposited. This brings

peace of mind but at serious cost - if more modest cash balances were

chosen, there would be an interest saving running to several hundred

million per annum.

It is not irrational to be a debtor while keeping cash on hand, up to a

point. The gap between what you pay to borrow and what you earn on

deposit is called the negative carry and is now up to three and four

percent per annum on some of the cash pile."

Ajai Chopra and an IMF delegation pass Anton

Rostas from Romania as they make their way to the Central Bank

for crucial talks with the government in Dublin on November 18th, 2010.

Photograph: Peter Morrison/AP

What is the Troika?

"The term Troika, which comes from the Russian meaning 'group of three',

was increasingly used during the eurozone crisis to describe the

European Commission, International Monetary Fund and European Central

Bank, who formed a group of international lenders that laid down

stringent austerity measures when they provided bailouts, or promises of

bailouts for indebted peripheral European states � such as Ireland,

Portugal and Greece � in the financial crisis."

"Capital markets are financial markets for the buying and selling of

long-term debt- or equity-backed securities. These markets channel the

wealth of savers to those who can put it to long-term productive use,

such as companies or governments making long-term investments. Financial

regulators, such as the UK's Bank of England (BoE) or the U.S.

Securities and Exchange Commission (SEC), oversee the capital markets in

their jurisdictions to protect investors against fraud, among other

duties.

Modern capital markets are almost invariably hosted on computer-based

electronic trading systems; most can be accessed only by entities within

the financial sector or the treasury departments of governments and

corporations, but some can be accessed directly by the public. There are

many thousands of such systems, most serving only small parts of the

overall capital markets.

Entities hosting the systems include stock exchanges, investment banks,

and government departments. Physically the systems are hosted all over

the world, though they tend to be concentrated in financial centres like

London, New York, and Hong Kong. Capital markets are defined as markets

in which money is provided for periods longer than a year.

A key division within the capital markets is between the primary markets

and secondary markets. In primary markets, new stock or bond issues are

sold to investors, often via a mechanism known as underwriting. The main

entities seeking to raise long-term funds on the primary capital markets

are governments (which may be municipal, local or national) and business

enterprises (companies).

Governments tend to issue only bonds, whereas companies often issue

either equity or bonds. The main entities purchasing the bonds or stock

include pension funds, hedge funds, sovereign wealth funds, and less

commonly wealthy individuals and investment banks trading on their own

behalf. In the secondary markets, existing securities are sold and

bought among investors or traders, usually on an exchange,

over-the-counter, or elsewhere.

The existence of secondary markets increases the willingness of

investors in primary markets, as they know they are likely to be able to

swiftly cash out their investments if the need arises.

A second important division falls between the stock markets (for equity

securities, also known as shares, where investors acquire ownership of

companies) and the bond markets (where investors become creditors)."

'Getting

ready for a successful return to the bond markets'

'The NTMA�s John Corrigan is cautiously optimistic about Irish plans to

tap the market'

One of the key issues facing Ireland post bailout is whether we can

achieve regular access to capital markets at sustainable interest rates

to enable the Government to continue to meet the day-to-day running

costs of the country.

We were locked out of markets in 2010 when the coupon on Irish sovereign

bonds became unaffordable and the country was forced into raising �67.5

billion from the EU and IMF via a bailout programme.

Three years on, and the National Treasury Management Agency is poised to

re-enter capital markets on a regular basis.

It has already had some success. In January it raised �2.5 billion in a

bond that will mature in 2017. The interest rate was 3.32 per cent. In

March the NTMA issued a 10-year bond at 4.15 per cent. This was the

first 10-year issue by the agency since January 2010, and reflected

improved sentiment towards Ireland as the economy continued to repair

itself slowly and the country complied with the conditions of the troika

bailout.

With Ireland exiting the bailout this month without the safety net that

a precautionary credit line might have provided, what are the NTMA�s

plans to tap the market in 2014?

Agency chief executive John Corrigan says we will have about �20 billion

in the kitty by the end of December. In addition, around �800 million

remains to be drawn down from the troika early in the new year.

�That should keep us going well into the first quarter of 2015,� he

says.

Bond redemption

Among other things, it will be used to meet a bond redemption in January

for just shy of �7 billion.

Next month will see the NTMA reveal its plans for fundraising next year.

�We�ll probably issue between �6 billion and �10 billion [next year],�

Corrigan explains. �We�ll announce in January what the complexion of

that is likely to be. Ideally, it will involve some auctions during the

course of 2014 because the challenge is achieving a regular return to

the markets on a sustainable basis.

�We raised �7.5 billion in the bond markets [in 2013] but that funding

was on an opportunistic basis. We sort of jumped out of the bushes when

we thought it was right. We need to get into a pattern that shows we

have regular access. That�s the key.�

The NTMA plans to meet with primary dealers in London this month to

gauge their views on Ireland�s return to capital markets. �It�s the

primary dealers who are dealing with the markets on a day-to-day basis.

They know what�s likely to travel. If we were to do a syndicated issue

in 2014 . . . five or so primary dealers would be drawn from this group

[in London].�

There will also be trades in short-term treasury bills, or T-bills as

they are better known. These are typically �500 million in size with

three-month maturities. Corrigan describes them as �tactical funding�.

Economy crashed

Irish bond yields are currently around 3.5 per cent, below the 4-4.5 per

cent level that we would have been paying before the economy crashed

when we were an AAA-rated country. This reflects the current low

interest rate environment globally. �What that tells you is that the

bond markets are dislocated for all the reasons that are well

rehearsed,� he says. �So it makes sense to lock in at the longer end

[longer-dated debt].�

Corrigan is more interested in the spread over German yields, which is

about 175 basis points. This is the risk premium attaching to Ireland at

present. �The spread of 175 over Germany is not for nothing. It�s not a

risk-free investment.�

Will the NTMA move early in the new year to secure funding while

interest rates are so low? �We�ll have to wait and see. You have to be

very sure-footed. You never say you�re going until you�re absolutely

certain you�re going.�

A key issue in a successful return to the markets would be a re-rating

by Moody�s of Ireland to investment grade. In September Moody�s changed

its outlook on Ireland�s sovereign rating to stable from negative but

stopped short of moving us from its Ba1 sub-investment grade, which

Corrigan says would have a number of benefits for us. We�re just one

notch away.

�It�s very important. The Asian investors, where we would have had a

good following [before 2008], have been largely sidelined by the fact

that Moody�s has us at sub-investment grade. And there are odd pockets

of investors around Europe as well whose mandates from clients would

only allow them to invest when the credit rating is investment grade

from the three main rating agencies. That�s the typical investment

mandate that you have in Asia and the Far East.�

The NTMA has been pounding the pavements in the past two months in Asia

selling the Irish story to investors. �Certainly there�s appetite and

it�s the marginal investor that can help your yield . . . so it is

important.�

Moody�s recently moved Portugal to a stable outlook and its eurosceptic

view appears to be softening. �We see that as a positive,� says

Corrigan. �It wasn�t necessarily conditions in Ireland that were holding

back Moody�s but they had a take on the euro zone as a whole that was

sceptical. We would be quietly hopeful.�

The NTMA has used Minister for Finance Michael Noonan to help sell the

Irish recovery story overseas. He regularly pops up on Bloomberg TV for

interviews and attends investor sessions where possible.

Fitch was the first ratings agency to soften its view of Ireland and

Corrigan believes the Minister�s appearance at a meeting with them in

Washington DC helped to seal the deal.

�He�s a straight talking man. That�s one of the small-country advantages

that we have. Ratings agencies wouldn�t normally get access to the

finance minister as they would with Ireland.�

It�s not all honey and jam. The general government debt is estimated to

stand at �206 billion by the end of this year or 124 per cent of GDP.

The cash interest cost of the national debt this year will be about �7.2

billion, rising to �8.2 billion in 2014.

What are the challenges that could scupper Ireland�s return to regular

market funding?

�There�s a lot of uncertainty still remaining in the euro zone, although

the white heat surrounding it has calmed down.

�We also have to see the unwinding of the quantitative easing in the

United States, and we saw a trailer earlier this year of how the market

might react if it�s not handled carefully.

�Then we have the [euro zone] bank stress tests towards the back end of

2014. The deferral of the [Irish] stress tests to coincide with the euro

zone-wide stress tests was seen as a positive by the investment

community because it meant we weren�t being picked for special

treatment. Nonetheless, there�s a risk there.

Primary surplus

�I don�t believe we�ll have an issue accessing the funds. The question

is over time to continue to run a primary surplus that will get the

debt-to-GDP level down to what is more acceptable to capital markets.

We�re committed to doing that anyway under the various EU protocols but

that would reflect itself then in a narrowing of the spread [with German

bonds].�

Corrigan has no regrets about the decision to exit the bailout without a

precautionary credit line in place.

�We didn�t need it anyway because if you got a credit line it only

applies for 12 months. We have the cash in the bank [for the next 12

months],� he says.

Hasn�t he changed his tune? After all, only a few months ago he was

talking about it being a �good club� for Ireland to have in its golf

bag.

�We would have discussed this with investors and with the ratings

agencies and they were very relaxed about it. They see us as having been

put through the ringer with stress tests and other troika measures.

�They see us as having delivered on most if not all of the troika

measures and we are in relatively good health.

�But we are cautious people and that prompted me to say that it would

have been a nice club to have in the bag. Overall, I think we�re in a

good place and have a good story to tell.�"

Trichet

letter revealed: ECB threatened to stop emergency funding unless Ireland

took bailout

Exclusive: �Secret� letter obtained by The Irish Times shows Brian

Lenihan was told to seek bailout

(The Irish Times - Nov 6, 2014)

The European Central Bank (ECB) explicitly threatened in late November

2010 to cut off emergency funding from the Irish banking system, unless

Ireland immediately applied for a bailout and agreed a programme of

austerity and bank recapitalisation.

The letter from then ECB president, Jean-Claude Trichet, to former

finance minister Brian Lenihan � marked �secret� � was sent on November

19th, 2010. A copy has been obtained by The Irish Times. Its publication

is due to be considered at a meeting of the ECB governing council today.

The letter states that the governing council of the ECB would only agree

to provide further emergency liquidity assistance (ELA) to the banks if

it received �in writing a commitment� from the government to apply

immediately for a bailout.

It said that the request for financial assistance had to contain a

commitment to budget cutbacks and a restructuring of the financial

sector.

Also, it said that the restructuring plan must include the provision of

the necessary capital to the Irish banking system and that the

government had to agree to underwrite the repayment of the ELA to the

Central Bank.

ELA was special funding provided to the banks who no longer were able to

draw down normal ECB lending. Around �50 billion had been extended to

Irish banks at the time � with additional funds approved by the ECB the

day before.

A failure to continue this funding would have threatened their ability

to stay open and provide cash to the public.

Swift response

The letter was sent the day after Central Bank governor Patrick Honohan

appeared on Morning Ireland to say Ireland had no option but to apply

for support. The ECB letter called for a �swift response� from the

government.

Two days later, on November 21st, the formal application for the bailout

was made.

The ECB council was due to consider the publication of the letter today,

and it is thought they may also release earlier correspondence.

The ECB would be expected to argue that its financial exposure to

Ireland and the risk that the money would not be repaid left it with no

option but to try to secure its position. Critics will say that the ECB

overstepped the mark in dictating to the government.

'Blog: The Troika's leaving, but we're under their thumb until 2034'

"It's often

overlooked but the Troika's entry to Ireland - and the terms

and conditions of the subsequent Memorandum of Understanding

between Ireland and its paylords - followed the negotiation

of the national Stability Programme with the European

Commission. That's the deal responsible for the 'Four Year

Plan' - where the general framework of every Budget until

2014 - was originally mapped out.

That programme - and bear with me here, because this is

where the terminology gets bonkers - is because Ireland is

currently knees-deep in an 'Excessive Deficit Procedure' (EDP).

In short, the gap between Ireland's income and its spending

became so pronounced in 2008 and 2009 that the European

Commission stepped in to take an overseeing role in how bad

we were doing. A slow process

The EU's rules dictate that this happens when the budget

deficit (i.e. the gap between spending and income) exceeds

3% of the total size of Ireland's economy. Basically - under

treaties Ireland has voted to accept - the Commission gets

to hang around and have input into the Budget process until

we get the deficit below 3% again. This year it'll clock in

at around 7.5%; next year it should be about 4.8%, and all

going well we'll make it to 3% in 2015.

But all of this means the Commission still gets a hands-on

role in scrutinising the shape of Budget 2015 until we get

back to the 3% mark. At current rates, that'll mean an

eighth successive austerity budget with adjustments of

around �2.5bn.